Significant structural and operational changes are afoot in the capital markets industry, with the US transitioning to a shorter T+1 trade settlement period from 28 May, 2024. There are concerns that the shortened settlement period in the US will create misalignment and friction with other capital markets around the world, such as the EU and UK, which are currently operating on a T+2 settlement period. One such example of where this misalignment will be apparent is in the trading of exchange-traded funds (ETFs) that contain globally-domiciled constituents, where the ETF will settle on T+1, but the underlying securities will settle on T+2.

As such, in order to stay aligned and reduce operational complexities, the EU and UK are exploring the potential of transitioning to a T+1 trade settlement period, with specialist task forces drawing up early-stage plans. Increasingly, from a UK perspective, it looks to be a case of ‘when’ and not ‘if’ the UK adopts T+1 trade settlement, whereas the EU is comparatively more hesitant. Findings from The European Securities and Markets Authority (ESMA) last month revealed reluctance in transitioning to a T+1 settlement period, citing how the costs may outweigh the benefits due to post-trade and inventory management issues and the degree of automation required. ESMA intends to deliver its final assessment to European policymakers in September 2024.

The UK is progressing toward a T+1 settlement period, with the prospective shift to T+1 being managed by the UK Accelerated Settlement Taskforce. Launched in the wake of the UK Government’s Edinburgh reforms in December 2022, the taskforce exists to explore the potential for faster settlement of securities transactions in the UK.

In March 2024, the taskforce revealed key recommendations for the UK’s prospective T+1 transition in a report, which, crucially, have been ‘accepted in full’ by the UK government:

The UK should commit to moving to a T+1 settlement no later than 31 December 2027.

The UK should explore collaboration with other European jurisdictions, with a view to coordinate in terms of transitioning to a T+1 settlement period.

The UK should establish a technical group comprised of cross-industry experts that helps determine the technical and operational challenges that need to be overcome to achieve T+1 by the end of December 2027.

The taskforce has since published a quarterly review, which will become customary up until the 2027 deadline, providing updates on the UK’s progression toward a T+1 settlement period. In particular, the update cites the importance of putting in place a settlement readiness plan by no later than 2025 to help ensure the prospective 2027 deadline is met, with plans already being put in place.

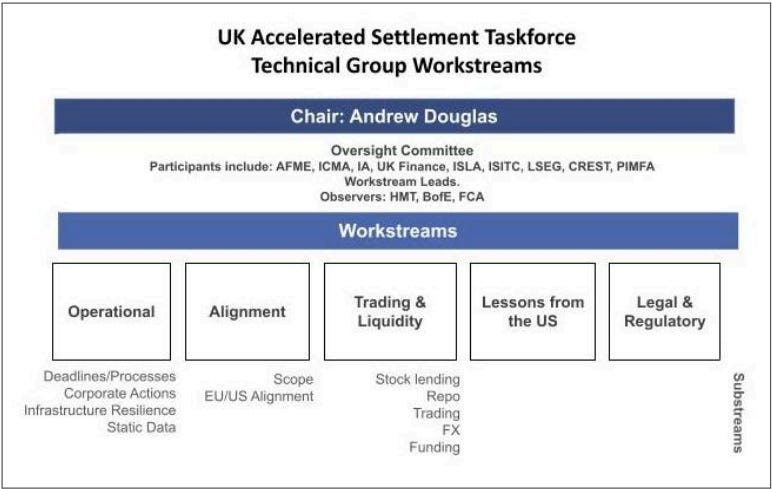

The report revealed that roughly 400 volunteers, representing 99 financial institutions are engaged in ‘technical conversations’ regarding the transition to T+1, while also revealing the establishment of five overarching workstreams tasked with the role of identifying the problems that need to be overcome if T+1 is to be implemented successfully. These five workstreams are Operations, Alignment, Trading & Liquidity, Lessons from North America and Legal & Regulatory.

As the model below shows, these high-level workstreams have established sub-streams that are focused on addressing specific challenges belonging to that particular workstream. For example, a key element of the operations workstream will be ensuring that UK firms’ trading systems are structurally fit for purpose when it comes to implementing a T+1 settlement period. It is down to the leaders of each workstream to report their individual findings to the wider group, which will be published in September 2024 for an industry consultation, ahead of final publication in December 2024. The final publication will confirm the transition date for the implementation of T+1 in the UK.

Source: Andrew Douglas, Technical Group Chairman, via LinkedIn

However, there are two caveats with respect to this transition date in the UK. One is what happens in the US with its own T+1 implementation, with the UK seeking to learn lessons from the US transition starting later this month. The other is what recommendations ESMA makes in its aforementioned September 2024 report, with the UK seeking a coordinated approach with the EU in order to keep alignment. However, this may be easier said than done. EU regulators have noted that the jurisdiction has multiple stock exchanges, clearing and settlement venues, making a switch to T+1 more complicated and lengthy than for a single jurisdiction such as the UK. If coordination cannot be achieved, taskforce chairman Charlie Geffen noted that the UK should ‘proceed in any event.’

Given it is a case of when the UK transitions to a T+1 settlement period, UK financial firms should now be giving some consideration to the inevitable T+1 settlement requirements and assess the wider impact of it on their business.

We look forward to keeping you updated with the forthcoming quarterly reviews regarding the UK’s transition to T+1 settlement.