FCA Consumer Duty Deadlines

31 July 2024 is the next compliance date for in-scope firms

In the UK, the Financial Conduct Authority (FCA’s) Consumer Duty regulatory framework sets higher and clearer standards of consumer protection across financial services and requires firms to put their retail customers' needs first. The Duty applies to firms dealing directly with retail customers in the UK or involved in the manufacturing and/or distribution of retail products and services to UK customers. Further, it applies to the regulated activities and ancillary activities of all firms authorised under the Financial Services and Markets Act 2000 (FSMA), the Payment Services Regulations 2017 (PSRs) and Electronic Money Regulations 2011 (EMRs), which includes broker-dealers.

In implementing the Consumer Duty framework, the FCA is seeking to address the following issues:

Poor value and customer service;

Products and services that do not deliver the benefits reasonably expected;

Misleading or difficult to understand information, and;

Behaviours that exploit vulnerabilities, inertia and biases.

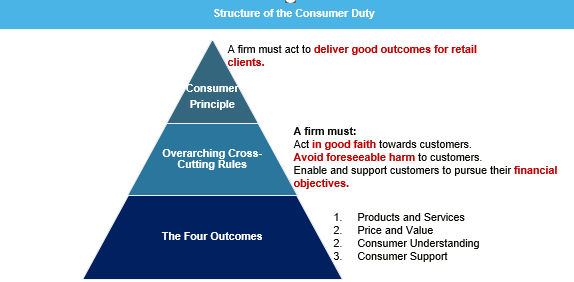

The FCA expects a significant shift in both culture, governance and behaviour from in-scope firms, ensuring that consumers experience four ‘good’ outcomes, which are fair prices and value, product quality, understanding and consumer support, as depicted below:

Source: GreySpark analysis

The Consumer Duty framework has been in the works for around two years, entering into publication by the FCA in July 2022, with in-scope firms’ board plans for implementation established in October 2022. In April 2023, firms involved in the manufacture and distribution of retail products completed reviews for existing open products. The implementation deadline, by which changes had to be made to existing open products and services to meet the Duty requirements, was 31 July 2023. For closed products and services, the implementation deadline of 31 July 2024 is one week away. This includes the requirement that there is and remains a reasonable relationship between the price customers pay and the benefits of the product or service.

To recap, a ‘closed product’ is defined as a product:

where there are existing contracts with retail customers entered into before July 31 2023; and

which is not marketed or distributed to retail customers (including by way of renewal) on or after July 31 2023.

An example may include an insurance product that was available to retail customers before July 31 2023 and where some of those contracts/policies remain active, but which are no longer available for purchase by new customers or renewal by existing customers. Firms with closed products are likely to include outsourcing providers and debt purchasers.

A full timeline of events regarding the Consumer Duty framework can be found below:

Source: GreySpark analysis

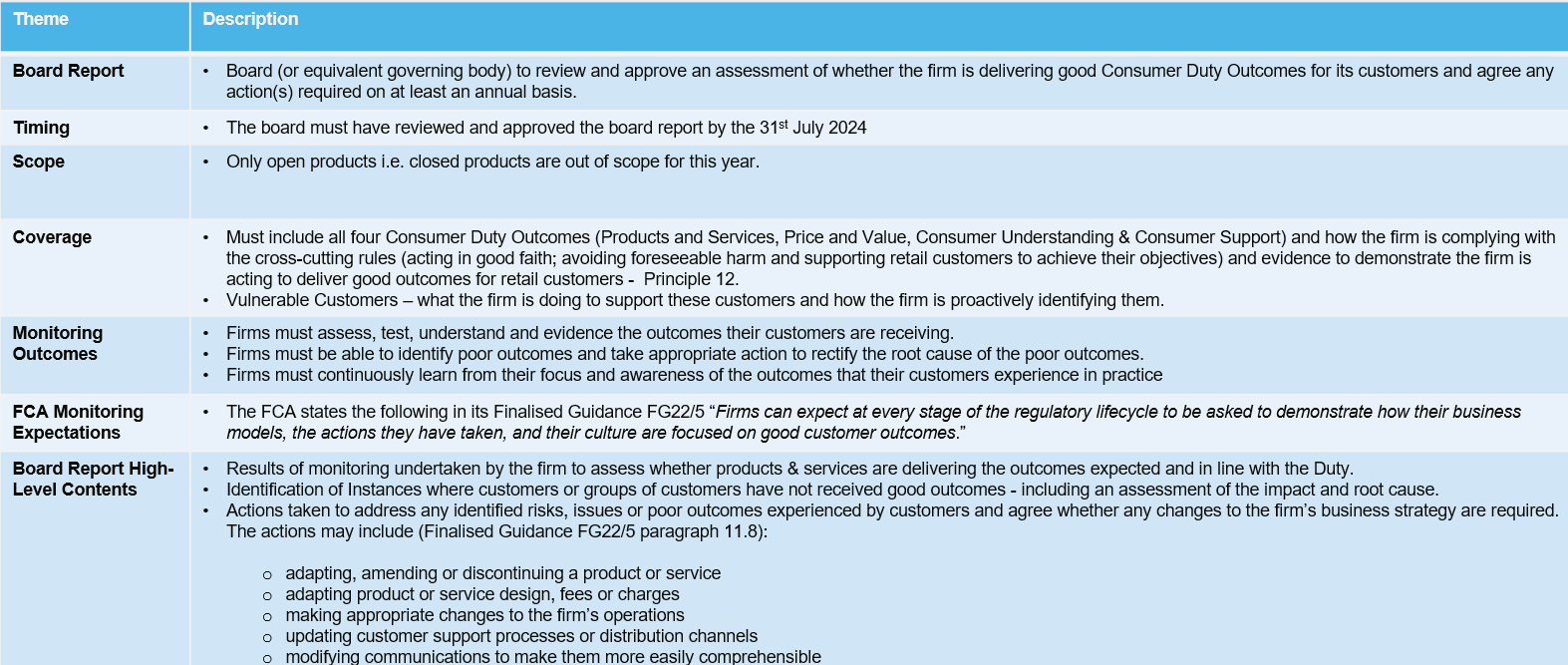

In addition, the firm in question must produce an Annual Board Report to consider whether it is delivering good outcomes for consumers. The Board will be required to scrutinise, review and confirm whether it is satisfied the firm is complying with the Duty. At the same time, the board will be required to ensure the Duty is embedded within the firm’s strategies and business objectives, with the outcomes becoming a central focus for risk and audit functions.

The board of the firm in question must have reviewed and approved the first annual Consumer Duty board report by 31 July 2024. The requirements for this year’s report can be found below (in large size, as appropriate):

Source: GreySpark analysis

With the 31 July 2024 deadline for closed products/services and the first annual board report under the terms of the Consumer Duty Act, in-scope firms should, if they haven’t already, be giving close consideration to the new requirements and modify their business models as appropriate.