Crypto Regulatory Overview

The EU's attempt to create the world's first comprehensive set of crypto regulations

Hello everyone and welcome to the latest edition of GreySpark Insights.

Please do not hesitate to contact us with any questions or comments you may have. We are always happy to elaborate on the wider implications of these headlines from our unique capital markets consultative perspective. Happy reading!

Image: Jocelyn Schuffenecker via LinkedIn

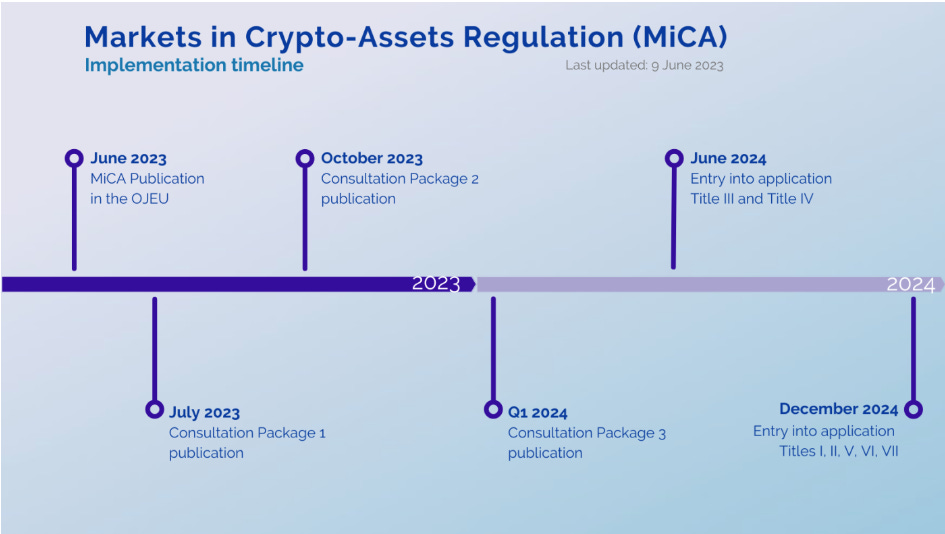

In June 2023, the Markets in Crypto-Assets regulation (MiCA) entered into force, becoming the first comprehensive regulatory regime, globally, that is tailored specifically to cryptoassets trading. The introduction of MiCA seemingly established the EU as the global pace setter when it comes to crypto regulation, and could set a precedent for what other regulatory frameworks could look like across other jurisdictions in the future.

MiCA aims to provide regulatory certainty and stronger protections for consumers in the crypto market without stifling innovation in the sector. MiCA covers cryptoassets that are not currently regulated by existing financial services legislation. The legislation creates key provisions for cryptoasset service providers that are issuing and trading cryptoassets — including asset-reference tokens and e-money tokens — covering transparency, disclosure, authorisation and the supervision of transactions. Ultimately, the MiCA framework will support market integrity and financial stability by regulating the provision of cryptoassets and by ensuring consumers are better informed about their associated risks.

In particular, MiCA seeks to establish mechanisms that ensure stablecoins are stable, provide enhanced transparency and prevent market players from creating excessive risk, while also ensuring that the assets under custody are protected. Interestingly, MiCA seeks to mitigate the environmental impact of cryptoassets by regulating crypto mining processes, which are typically a major source of greenhouse gas emissions.

Who are the regulators?

the European Securities and Markets Authority (ESMA)

How are cryptoassets regulated by MiCA?

The terms of MiCA are applicable to three types of asset:

Asset-reference tokens — A type of cryptoasset that purports to maintain a stable value by being ‘pegged’ to the value of another asset, including commodities, other cryptoassets or fiat currencies;

E-money tokens — A type of token — for example, a stablecoin — that is pegged to the value of a single fiat currency;

Other tokens, such as utility tokens — A utility token is a blockchain-based token that is used to access a particular crypto network.

MiCA provides the following requirements for offering these cryptoasset types to the public and for their admission onto trading platforms for cryptoassets, along with a set of requirements for cryptoasset service providers:

Transparency and disclosure requirements for the issuance of cryptoassets on a trading platform. The issuer must produce and distribute a white paper in relation to the asset, which must contain rights, obligations and risk-related information, and it cannot constitute false advertising.

Requirements for the authorisation, supervision and governance of cryptoasset service providers. These requirements include a profile of the existing activities and products offered by any service provider(s) that fall within the scope of MiCA’s rules.

Requirements for the protection of the holders of cryptoassets in terms of the issuance the products and in terms of how they are offered to investors, inclusive of terms detailing the admission of trading in cryptoassets on relevant brokerage platforms.

Requirements for the protection of clients of cryptoasset service providers.

Measures to prevent insider dealing, unlawful disclosure of inside information and market manipulation related to cryptoassets trading to ensure the integrity of the overall marketplace.

Who do the regulations apply to?

Entities covered by MiCA are called Crypto-Asset Service Providers (CASPs) in the regulatory text, and they include:

Custodial wallet(s) providers;

Exchanges for crypto-to-crypto transactions or crypto-to-fiat transactions;

Platforms with crypto trading functionality;

Cryptoasset investment advisory firms and crypto-portfolio managers (including asset managers, wealth managers, credit institutions, market operators, e-money institutions, UCITS management companies and alternative investment fund managers).

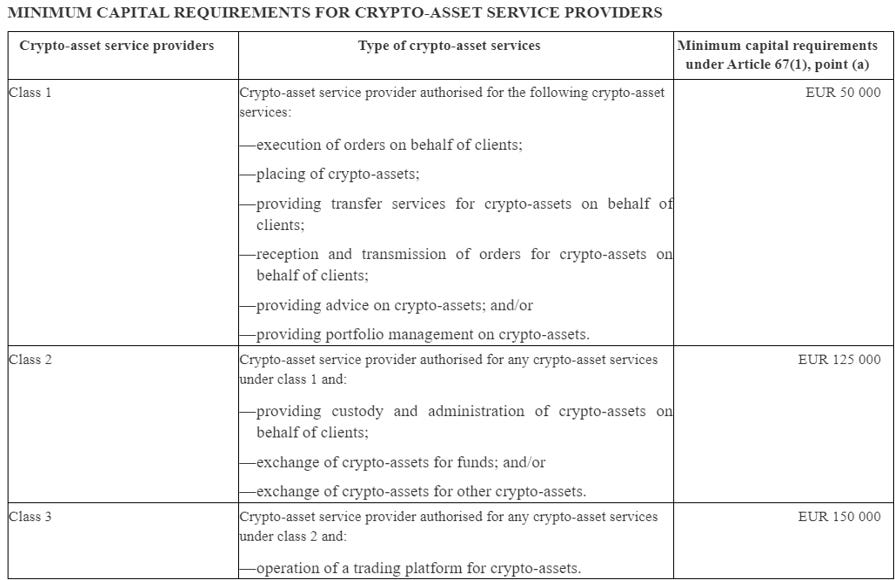

Those in-scope entities must achieve minimum capital requirements for the specific service that they provide, as the table below shows:

Regulatory issues and challenges

Authorisation & Notification — Companies or firms will need to classify their existing holdings of cryptoassets according to MiCA’s definitions (i.e., e-money tokens, asset-referenced tokens). This may require a comprehensive internal review process.

Data Management — MiCA is likely to require enhanced reporting and transparency to bring the crypto trading industry’s pre- and post-trade reporting requirements in line with likewise standards applied to markets for other, fiat-centric instruments or products. This stipulation, if approved as an addendum to the existing regulatory langauge, could potentially increase operating costs for in-scope firms. According to Coindesk, MiCA could create ‘one-off compliance costs’ ranging between USD 3.2mn and USD 19mn.

Consumer & Investor Protection — The production and distribution of white papers is a key part of MiCA’s consumer protection protocol, and is a requirement for all in-scope firms that provide the three types of token outlined above.

Environmental Impact — Cryptoasset market participants must ensure relevant technology is climate-friendly in accordance with the EU’s Green Deal, and will therefore be obliged to disclose their environmental and climate footprint.

Custody Liability — Providers of custodian wallets will be liable for damages or losses caused by hacks or preventable failures. New liability rules are also specified for custodians that hold asset-referenced tokens.

Loopholes & Blind Spots — The practical difficulty that MiCA faces from an enforcement perspective is where lines are drawn between regulated financial products and non-regulated financial products. For example, MiCA rules do not cover some emerging trends in the crypto space such as non-fungible tokens (NFTs) and decentralised finance (DeFi) projects because they largely operate without intermediaries. DeFi projects are typically governed by smart contracts, which are built and deployed without their creators ever exposing their identities. This secrecy can lead to the development of malicious software and crypto scams out of sight from regulators. As a result, it is likely that ESMA will need to adjust the terms of MiCA to bring DeFi into scope of MiCA in order to protect market participants. ESMA is reportedly ‘looking into’ the DeFi ecosystem and considering ways to bring it into scope.

Additionally, a loophole in the MiCA legislation could allow offshore companies to continue to serve EU customers without extra regulation in a process known as reverse solicitation. Reverse solicitation exists because regulators do not want to block domestic firms receiving expertise from overseas. MiCA requires companies targeting the EU market to register with a local regulator, who then checks on their governance and marketing to ensure that potential investors are not misled. However, this can open the door to market abuse and lead to a lack of transparency because these entities ultimately have more regulatory flexibility than in-scope, domestic firms. For example, potentially bogus companies like FTX, based in the Bahamas, would still be able to serve EU-based clients without extra regulation. Therefore, the MiCA regulations still have much to answer for in terms of clarity and inclusivity.

Regulatory horizon

MiCA initially entered into force in June 2023 and is succeeded by three consultation packages that outline a host of technical standards and mandates:

1st package — Technical standards on issues including CASP Authorisation, information requirements and conflicts of interest;

2nd package — Various mandates including business continuity mandates, public disclosure of information and order book record keeping;

3rd package — Remaining mandates including market abuse, investor protection and order book record keeping.

MiCA rules on the provision of cryptoasset services are set to enter into full application in December 2024. MiCA grants EU member states the ability to allow entities already providing cryptoasset services within their borders to continue providing those services between December 30, 2024 until July 1, 2026 without a MiCA licence. This means that holders of cryptoassets and the clients of cryptoasset service providers may not benefit from full rights and protections afforded to them under MiCA until as late as July 1, 2026.

Why not head over to our website and take a look at our latest insights post. You can view this here!